Optimizing Educational Excellence: A Guide to Charter School Budgeting Best Practices

“A budget is telling your money where to go instead of wondering where it went.” – John Maxwell

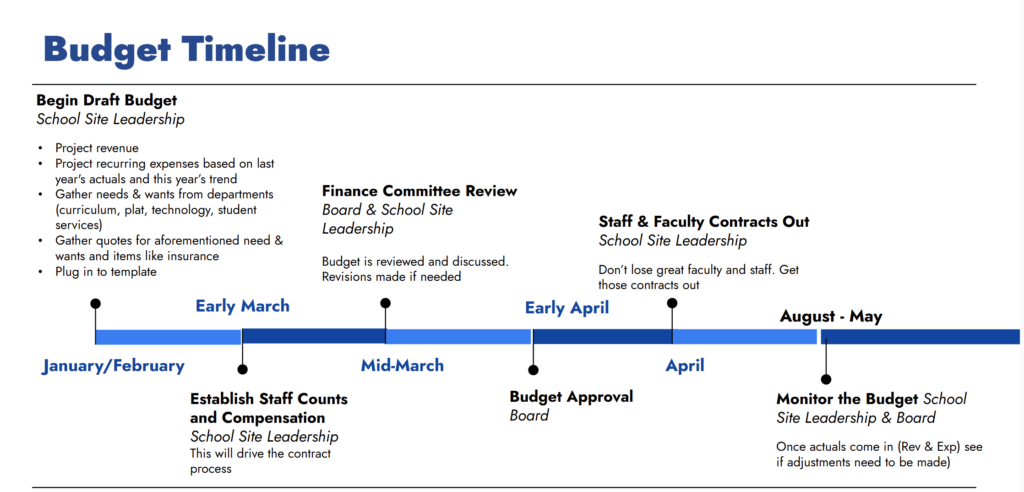

As we enter into spring, charter schools should not only focus on preparing for the upcoming state assessments but also begin the budgeting process for next year. A sound budgeting process helps school leadership plan and manage financial resources efficiently while providing a roadmap for allocating funds to various activities and programs to achieve organizational goals. A budget also provides schools financial stability as it enables proactive decision-making and risk management.

Over the past ten years, I have helped schools of all sizes and programmatic needs strategically develop budgets that help effectively allocate resources while building a strong foundation for long-term financial sustainability. While respecting the unique needs of each school and model, there are some underlying tenets of budgeting I recommend:

Start Early. Start NOW!

While most authorizers do not request the board-approved annual budgets until fall, many decisions for the upcoming school year – such as staffing, compensation, and purchasing– are made during spring and summer. Because a budget serves as the governing board’s directive to school leadership as to how to allocate funds, it is important to start the process prior to the time these decisions need to be made.

It is recommended that an initial balanced budget is drafted and taken to the governing board in early spring in preparation for the hiring season so that school site leadership knows the positions and the compensation that they can offer. Towards the end of summer, once student enrollment is better known, hiring is (hopefully) complete and most purchases are made, the school may want to consider a revision if there are significant variances between what was projected and what has occurred. If actual expenses exceed the projections, resources will need to be reallocated to maintain a balanced budget.

Progress through a Collaborative Process

More brains are better than one. Include your various school-site leaders in the process to provide input on the needs in their areas. Reach out to your curriculum team, facilities manager, technology gurus, food services staff, etc. to develop their list of their Must Haves and their Nice to Haves – this also includes any staffing needs/wants they may have. This collaborative approach not only establishes a transparent process, but it also helps manage expectations. Money is finite, and sometimes departments don’t understand why they may not have certain things or additional staff. A working budget template is a powerful tool in helping the entire team establish priorities and have ownership in the decision-making process.

Live within your Means

Governing boards should never approve a budget that is not balanced. While this seems obvious, my team and I have attended quite a few board meetings where governing boards are approving budgets that present a deficit. Not only should the budget balance, but it is also recommended that 5% is set aside for reserves. This can help absorb any unanticipated expenses or expenses that exceeded initial projections. Financial stability is a cornerstone of successful charter schools. Leaders should prioritize building and maintaining adequate reserves to weather unforeseen challenges or economic downturns. Establishing a reserve policy and regularly reviewing its adequacy ensures the school’s long-term sustainability.

After establishing conservative projections in revenue, carve out your “non-negotiables.” These are your required costs such as lease or bond payments, insurances, utilities, etc. Use actuals as much as possible, then use historical numbers, such as the previous year’s budget-to-actual report, to project future expenses. Utilizing what is left, the budget team should strategically allocate expenses according to the organization goals beginning with the Must Have lists and hopefully getting to the Nice to Have lists.

I emphasize the word process as it often takes multiple attempts to balance the budget. Teams will need to look closely at areas where expenses may need to be reduced. Yet don’t forget about ways to increase revenues as well in addition to aggressive student recruitment. After school or summer programs and pre-kindergarten programs are two ways, we have seen schools successfully increase revenues.

Once the budget team gains consensus on the annual budget, bring it to the board for approval.

Monitor Monthly

However, the journey does not end there; ongoing vigilance is essential. Monthly reviews and updates, aligned with a budget-to-actual report, enable school leaders and governing boards to adapt swiftly to changing circumstances.

A budget-to-actual report should be reviewed monthly to regularly assess spending patterns ensuring resources are optimally allocated. Begin by making sure your budget and your chart of accounts utilize the same Red Book codes so that budget-to-actual reports can easily be generated and deciphered. If the general ledger code on the chart of accounts aligns with the budget, it is easy to see how spending is trending. If a report is generated after October 31st revenue and expenses are logged, most expenses should be trending at or below 33.33% of the projected annual budget. In some cases, like technology or textbook purchases, it is likely that the expenses exceed 33.33% because those annual purchases typically occur prior to the opening of school, so it’s acceptable if it was trending at 84%. However, if your administrative salaries are trending at 65% in October, questions should be asked as the school is on a course to significantly overspend in that category. If a position was added beyond what was budgeted, adjustment will need to be made – either cutting the position or reallocated money from another line.

It is not uncommon for schools to revise the budget after the October FTE survey and again after the February FTE survey. This gives schools the opportunity to recalibrate revenues after actual enrollments and FTE recalculations are reflected and expenses can be adjusted based on actuals and reallocated as needed.

In conclusion, the art of budgeting for Charter Schools extends far beyond numbers on a spreadsheet. It is a dynamic process that demands foresight, collaboration, and adaptability. As we embrace the spring season, let us embrace the opportunity to fortify our schools financially, laying the groundwork for a flourishing future in education.